January 2024 – After a two-plus yearlong real estate roller coaster, Park City Realtors are experiencing a market that many characterize as “closer to normal” than we have seen in recent quarters. Instead of focusing on post-Covid recovery, agents are more inclined to talk about a stable market with continuing moderate price appreciation and growing inventory.

The current market is probably being affected by higher interest rates and somewhat reduced inventory more than by any Covid hangover.

The inventory of available homes is approaching a healthy level having peaked in late summer at nearly 1,800 properties for sale. In the last full year before the Covid-crash, PCMLS averaged 2,100 listings each month. Sales prices have stabilized with single-family homes within Park City limits selling for slightly less than they did a year earlier, and median prices in the Snyderville Basin are up just single digits year over year.

With inventories returning to a more normal level, and competition for available properties still running strong, market times and absorption rates (the length of time it would take to sell all current inventory based on the current rate of sales) are also remaining steady.

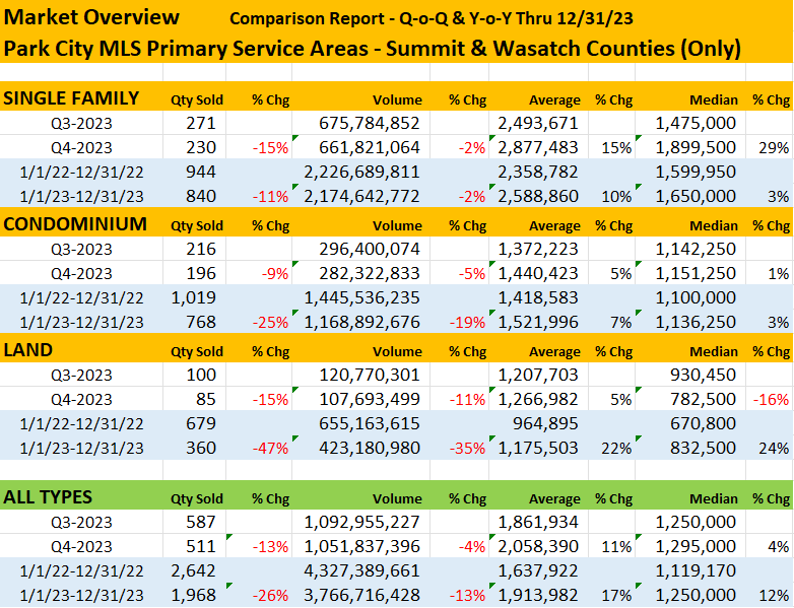

Sales totals for single family homes in Summit and Wasatch Counties for all of 2023 were down just 2% from 2022. Prices remained steady to up slightly. The median home sale price in the PCMLS primary market area increased just 3% for the year ending 12/31/23 vs. the same period ending 12/31/22. The short term measure of quarterly median price increases presages to some the direction consumers might see for both sales prices and volume in the year ahead. But Park City is a highly seasonal market and many others point out that comparing one quarter to the next is not a valid predictor of a future trend.

- The wild price swings that were prevalent the past couple of years have moderated. Average prices of single-family homes in Park City proper grew only 1% over last year. The median sale price for a single family home in the city actually declined 5% to $3.7 million.

In Summit and Wasatch Counties, the rate of sales (number of units sold) dropped 11% for single family homes and 25% for condominiums, from the full year prior. Sales declines across the region were attributed to fewer listings than demand could handle.

Park City is very much a community of neighborhoods. Prices and availability vary widely from one neighborhood to the next.

For single family homes, four of the five major areas that make up the greater Park City market showed drops in units sold from 2022to 2023. The exception was in the Snyderville Basin, where unit sales increased 4%. Within the central neighborhoods, Jeremy Ranch was the market leader in sales units, closing 34 sales, 42% more than last year.

Condo sales across the primary market range followed a pattern similar to single family homes. Year-over-year sales units increased in Heber Valley and around the Jordanelle by 33% and 13%, respectively. Closer in, condo unit sales in Park City and Snyderville dwindled, down 19% and 48% respectively.

Prices, however, were mixed across these two areas. Within the Park City limits, the median sale price rose 8% to $1.6 million. In the Snyderville Basin, the median sale price dipped just under $1 million, down 8%.

Comparing the 12 months ending December 31, 2023, to the same period ending in 2022:

- Residential inventory (single-family and condo) year-to-date is showing signs of recovery after a lengthy period of declines. At the end of December 2022, there were just 738 residential listings for sale in the entire PCMLS coverage area. On December 31, 2023, that number had grown to 880, almost 20% more.

- The market picked up some momentum heading into the last half of 2023. In the seven months from June thru December, PCMLS members signed 1,260 residential purchase contracts, 20% more than the previous year (1,054).

- With New Listings running slightly higher than Pending contracts, inventory is being replaced faster than it is selling. For the year ending 12/31/23, 2,915 listings were added to the system. For the same period only 2,031 were put under contract. That’s 884 more listings added than contracts written, which hasn’t been seen in quite some time.

Single Family Homes

The number of homes sold in 2023 across the primary market area (Summit & Wasatch Counties) was only 11% less than in 2022, confirming that the wild market swings we saw during the Covid crisis are well behind us.

A slight increase (3.1%) in the median sales price to $1.65 million confirmed that a great deal more stability has returned to the market than we have seen in quite some time. All indications are that stability will continue into 2024.

Highlights of the single-family home market:

- Within Park City limits, total unit sales were down 11% to 102 units. Sales volume declined 10% to $476 million in the past 12 months.

- The median price of a single-family home within Park City limits fell 5% to $3.69 million.

- Only 27 homes have sold in the popular Old Town area in the past 12 months. The median price dipped slightly to $3.5 million.

- Snyderville Basin residences followed the prevailing market with sales volume (down 15%) on a modest gain in the overall median price up 7% to $2.3 million.

- Market activity across the Snyderville Basin varied considerably between neighborhoods. Canyons Village, Sun Peak, Kimball, and Jeremy Ranch all saw increased sales which helped make Snyderville the only major area to see growth in sales volume, average price and median price.

- Silver Creek South and Promontory had the largest median price gains, 34% in each area. The median price of a Promontory home is now above $4 million.

- Canyons Village held on to crown of “most expensive area” with a median price once again topping $10 million.

- Among the outlying areas, the Jordanelle area had the lowest volume of sales (only 76 this year, down from 149 last year) probably because the median price nearly doubled during that time. More and more luxury homes are coming to market in anticipation of the opening of the new Mayflower ski resort, pushing the median sale price above $3 million.

Despite fluctuations in the regional markets, single-family sales activity in the primary market area was down 11% compared to the year prior. Single digit appreciation in sales prices kept the total sales volume within 2% of last year’s.

| Single Family Y-o-Y Summary End of Q4 2023 | Qty Sold | % Chg | Sales Volume | % Chg | Average Price | % Chg | Median Price | % Chg |

| Park City | 102 | -11% | 476,010,983 | -10% | 4,666,774 | 1% | 3,687,500 | -5% |

| Snyderville Basin | 290 | 4% | 963,040,669 | 16% | 3,320,829 | 11% | 2,262,500 | 7% |

| Jordanelle | 76 | -49% | 266,879,030 | -16% | 3,511,566 | 65% | 3,175,000 | 94% |

| Heber Valley | 247 | -1% | 339,341,217 | 1% | 1,373,851 | 2% | 940,803 | -4% |

| Kamas Valley | 81 | -22% | 94,136,771 | -44% | 1,162,182 | -28% | 965,000 | -23% |

| Total Primary Market Area* | 840 | -11% | 2,174,642,772 | -2% | 2,588,860 | 9.8% | 1,650,000 | 3.1% |

| Total Overall MLS Area | 985 | -9% | 2,337,382,868 | -2% | 2,372,978 | 7% | 1,455,000 | -1% |

* Primary Market totals include only Summit and Wasatch Counties.

Condominiums

- The Condo market in the Old Town neighborhood paralleled the single-family numbers, with unit sales and volume down. The median price of a condominium sold in Old Town was flat at $1.2 million.

- Price gains were evident in all neighborhoods, with Upper Deer Valley leading the gainers with a 45% median increase to more than $3.6 million.

- In the Snyderville area, perennial volume leader Canyons Village suffered a steep decline in sales, with units and volume both down over 50%. Canyons Village accounts for more than 65% of all sales in Snyderville, so those declines brought down the overall area performance.

- In Wasatch County, (areas where 10 or more sales are reported) Jordanelle Park demonstrated a trend we expect to see more of in the future – new resort activity stimulating sales and raising prices. Condo unit sales were up 63%, pushing sales volume to more than double 2022’s excellent performance.

| Condominium Y-o-Y Summary End of Q4 2023 | Qty Sold | % Chg | Sales Volume | % Chg | Average Price | % Chg | Median Price | % Chg |

| Park City | 232 | -19% | 526,425,756 | -7% | 2,269,076 | 14% | 1,612,500 | 8% |

| Snyderville Basin | 256 | -48% | 341,004,039 | -46% | 1,332,047 | 4% | 987,285 | -8% |

| Jordanelle | 234 | 13% | 261,892,380 | 16% | 1,119,198 | 3% | 1,064,782 | 9% |

| Heber Valley | 44 | 33% | 38,422,000 | 77% | 873,227 | 33% | 581,000 | 17% |

| Kamas Valley | 2 | -50% | 1,148,500 | -48% | 574,250 | 3% | 574,250 | -3% |

| Total Primary Market Area* | 768 | -25% | 1,168,892,676 | -19% | 1,521,996 | 7% | 1,136,250 | 3% |

| Total Overall MLS Area | 820 | -22% | 1,196,486,021 | -18% | 1,459,129 | 5% | 1,060,982 | -1% |

* Primary Market totals include only Summit and Wasatch Counties.

Opinions and Observations

What do Park City agents see coming in the next few months? Here are a few observations about the important market results that point the way, coming from those with their fingers on the pulse of the market.

- Interest rates affect sales in various neighborhoods very differently. In Pinebrook and Jeremy Ranch, where the bulk of the inventory is conventional family homes, many buyers need financing. With higher interest rates, that financing is harder to rationalize. In other areas, predominantly vacation or second-home inventory, more sales are to cash buyers, making interest rates irrelevant.

- In areas where it looks like prices dropped significantly (Promontory for example showed a 22% median sale price drop quarter-over-quarter) it’s important to look at the individual properties that made up that price decline. In Promontory, again as an example, it was not an overall market decline but an increase in the number of smaller, less expensive homes that sold that brought down the median. Buyers are encouraged to ask their Realtor to interpret the numbers rather than paint any area with a broad brush.

- The price of new construction (measured by price per square foot) has not changed demonstrably from pre-Covid levels to this past year. Material and labor shortages have been mitigated.

- November and December are traditionally slower months, but this year for some reason the number of “walk ins” is up. Visitors to Park City who plan their vacations around the opening of ski season are more and more interested in buying a second home for recreational purposes.

- The Park City market has been and will continue to be highly segmented, with each neighborhood having unique values and unique pricing trends. Even within one neighborhood, prices may vary widely based on many factors. Hyper-local knowledge is becoming more important to the buying (and selling) process.

- We continue to see significant interest in reselling vacant lots that were purchased two to three years ago. Many potential homeowners bought lots thinking they would build their own dream house, only to become discouraged by the short supply of building materials and/or labor to make the build. Those lots are slowly coming back on the market now.

Comparing Market Segments year over year:

| 2022 | 2023 | Changes Year over Year | ||||

| Units | Volume | Units | Volume | Units | Volume | |

| SFH | 1,082 | 2,395,268,076 | 985 | 2,337,382,868 | -9% | -2% |

| Condo | 1,049 | 1,462,571,235 | 820 | 1,196,486,021 | -22% | -18% |

| Land | 724 | 708,313,015 | 404 | 459,031,490 | -44% | -35% |

| TOTAL | 2,855 | 4,566,152,326 | 2,209 | 3,992,900,379 | -23% | -13% |

| Res Combo | 2,131 | 3,857,839,311 | 1,805 | 3,533,868,889 | -15% | -8% |

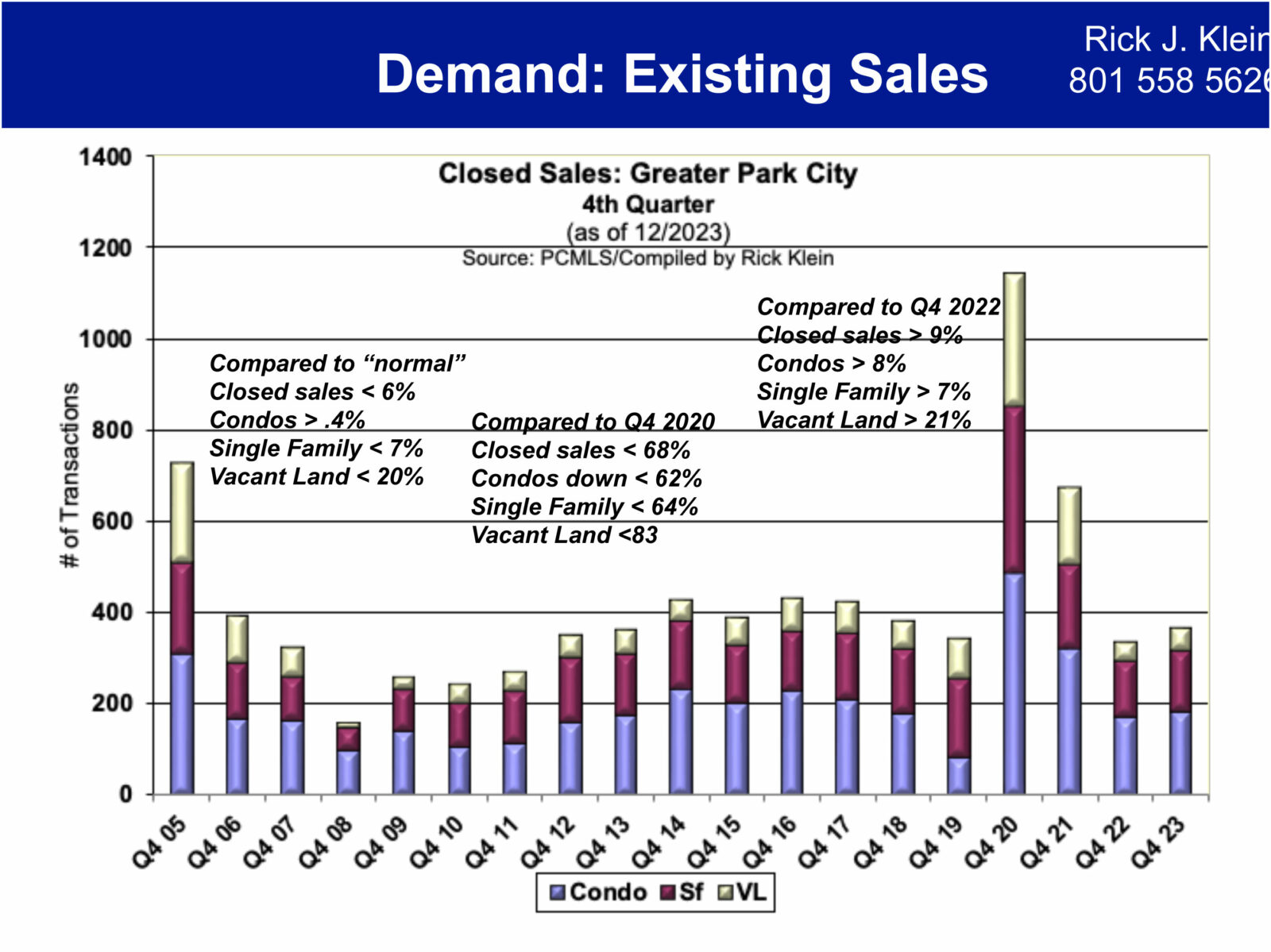

Despite all the red numbers (declines) in unit and volume of the most recent 12 months compared to the previous period, if we look at fourth quarter numbers compared to Q4 in prior years, the report is optimistic. Although total sales in Q4-23 are markedly below the same quarter in either 2020 or 2021, they are only slightly lower than the average of the “normal” period from 2013 to 2019. (Charts and observations courtesy of Rick Klein.)

The Park City market continues to appreciate as sale prices continue what has been a 10 year ascent ever higher.

Looking at combined residential sales, the chart at the right shows the steady rise in prices since the market downturn from 2008 to 2012. The increase from 2020 to 2023 was about 52%, significantly higher than our historic norm of 6.8% annual growth. In the most recent 12 months, the increases have been barely one-quarter of that rate, 6.6%. This is much closer to our usual or “normal” rate of appreciation. Real estate in the Wasatch Back continues to look like a very strong investment over the long run with no signs of slowing down.

What are the key takeaways from this quarter’s numbers?

- Since the all-time sales record reached in Q4 2020, sales slowly diminished and fell below the “normal” level by Q4 2022. Sales have slowly improved this past year with Q4 now within 6% of pre-Covid normal. Given our strong Q4 pending sales and the likelihood mortgage rates will decline next year, 2024 appears most promising.

- Inventory of available properties has improved significantly over the past two years, but still remains 25% less than pre-pandemic levels. Much of this improvement is due to new product. At the start of 2024, more than half of the residential listings in the greater Park City area are new construction.

- Pricing is not consistent across the broader market. Condo prices overall, for example, in Park City proper showed an 8% median price gain. However, most areas were either flat or showed a slight decrease. The large gains seen in Upper Deer Valley and Empire Pass accounted for the overall increase. Similarly, single family homes in the Snyderville Basin prices show an impressive overall gain (7%). But of the 12 neighborhoods in the Basin, seven saw price declines. These were more than offset by huge price increases in Silver Creek South and Promontory (34% each) that accounted for one-third of all Basin sales.

- Bottom line: our market is in transition, it is nuanced, and more than ever buyers and sellers need knowledgeable agents who understand the neighborhoods and the trend differences between them.

Real estate in the Wasatch back consists of highly segmented markets with nuances that vary significantly from one neighborhood to another and one house to another. Comparisons are hard to read on paper due to the unique features of individual properties, such as amenities, condition, style, location, age, view, and inventory. Buyers and Sellers are advised to contact a local Park City Board of REALTORS® Professional for the most accurate, detailed, and current information.

Overall, how did the local market fare? The tables that follow show two ways of looking at the market: For each area, the first two lines (white) compare the results of the 3rd Quarter 2023 to 2nd Quarter 2023.

The two lines in Blue compare the total year-long results on a rolling year-over-year basis for the period ending December 30, 2023.

(Note: only areas with 10 or more sales are considered in the reporting.)